As the economic landscape continues to evolve, it is important to understand the forces shaping the markets. This quarter's review examines key developments—from monetary policy and inflation to global events—and offers perspective on what they may mean for investors in the months ahead.

Executive Summary

A wave of high-profile Initial Public Offering (IPOs) announcements captured investors’ attention during the second quarter, though history suggests that newly public companies often face near-term challenges. A leadership transition at the Federal Reserve (Fed) could alter both policy communication and key policy priorities, potentially increasing market volatility. More broadly, inflation remains a key challenge, driven by tariffs, energy dynamics, and demand linked to the AI buildout. With the labor market stabilizing and policymakers retreating from an easing bias, a rate cut now appears highly unlikely. While easing geopolitical tensions may help moderate some price pressures, investors continue to face a backdrop of persistent inflation risks and a less accommodative monetary policy environment.

Blue Trust Insights

IPO FOMO

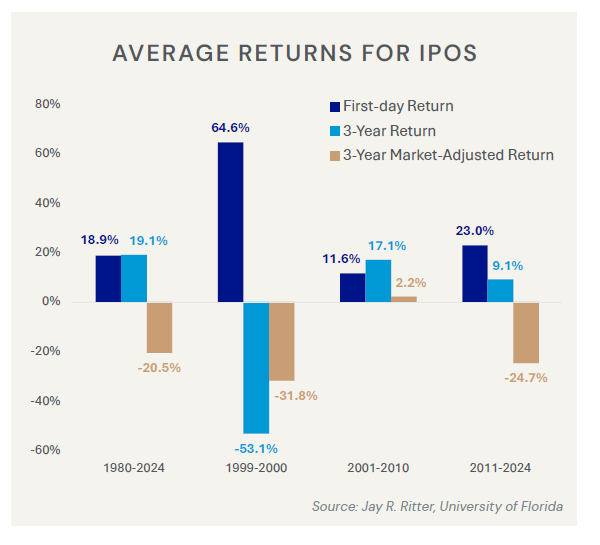

With several of the largest IPOs in history expected to come to market this year, it is no surprise that investor attention toward new equity offerings has intensified. Near the end of the quarter, SpaceX completed what is now the largest IPO on record, while one of the most prominent players in artificial intelligence (AI)—Anthropic—is expected to go public later this year.

A common quip among investors is that IPO stands for “It’s Probably Overpriced.” While the remark is made in jest, it carries some truth. Research from the University of Florida shows that since 1980, IPOs have generated an average first-day return of about 19%.1 However, the average three-year market-adjusted return—measured against the broader U.S. market—falls to -21%. Facebook (now Meta Platforms) illustrates the point. Despite its 2012 debut being one of the largest and most anticipated IPOs in history, the stock fell more than 30% during its first year even as the broader market advanced.

In short, history suggests that patience is often rewarded as enthusiasm surrounding IPOs tend to fade in the months following their debut. While many of the companies expected to go public this year have compelling long-term growth prospects, current valuations appear elevated. As a result, we believe a cautious approach is warranted. You can read our recent blog post discussing IPOs here.

A Changing of the Guard at the Federal Reserve

Jerome Powell concluded his eight-year term as Fed chair in the second quarter, ushering in new leadership under former Fed Governor Kevin Warsh. His tenure ended amid growing tension with President Trump, who criticized the Fed for moving too slowly on rate cuts. Despite those disagreements, U.S. equities delivered annualized returns of more than 15% during Powell’s tenure.

The Fed’s most significant misstep under Powell was its delayed response to the post-pandemic inflation surge. While the characterization of inflation as “transitory” remains a notable policy error, the Fed was not solely responsible for rising prices. Unprecedented fiscal stimulus was a key driver of inflation, while other pandemic-era policies also played a role.

Warsh now faces a similar challenge. Much of today's inflationary pressure stems from factors outside the Fed's direct control, including tariffs and higher energy costs, limiting the effectiveness of traditional monetary policy tools.

A New Philosophy

Fed chair Warsh has framed his approach as a regime change, arguing the institution has drifted from its core mission and weakened its credibility in the process. His vision is decidedly old-fashioned: less forecasting, fewer public pronouncements, and more robust internal debate.

A central element of Warsh’s critique is the Fed’s decision-making process. While the committee structure is designed to improve outcomes through diverse perspectives, he argues it can foster consensus-driven thinking that discourages dissent and encourages conformity. In his view, this “groupthink” contributed to the Fed’s misreading of post-pandemic inflation. In response, Warsh aims to encourage a wider range of viewpoints and more rigorous internal debate.

Warsh has also called for a more restrained communication strategy. He believes forward guidance can lock policymakers into outdated expectations and that less frequent public commentary could provide greater flexibility in responding to evolving economic conditions. This view was on full display at his first meeting as chair, as the post-meeting statement removed reference to forward guidance, and Warsh declined to submit a projection for interest rates.

Shrinking the Balance Sheet

Another pillar of Warsh’s agenda is reducing the Fed’s footprint in financial markets. During his Senate confirmation hearing, he described interest rates as a “fairer” tool, preferring to ease policy through rate cuts rather than balance sheet expansion, which he believes disproportionately benefits asset holders.

Since the 2008 financial crisis, repeated rounds of large-scale asset purchases have significantly expanded the Fed’s balance sheet and helped to suppress long-term interest rates, making government deficits more sustainable. Warsh has criticized the evolution of these programs from emergency measures into routine policy tools.

A reduced Fed presence in asset markets could place upward pressure on long-term interest rates, particularly if large fiscal deficits persist. However, Warsh has indicated that any effort to shrink the balance sheet would be communicated well in advance and implemented gradually in coordination with the Treasury Department.

Who Buys the Debt?

Scaling back the Fed’s asset purchases raises a key question: who replaces that demand? Private investors would need to absorb a greater share of government debt, making markets more sensitive to economic conditions as a large price-insensitive buyer exits.

Several forces could help fill the gap. First, demographics may support Treasury demand, as aging investors tend to shift portfolios toward fixed income. Given the concentration of wealth among older generations, even modest reallocations could meaningfully boost demand. Second, stablecoins—which are typically backed by Treasury securities and other highly liquid assets—are expected to become an increasingly important source of demand. While they are unlikely to replace the Fed as a buyer of longer-dated securities, they could provide a persistent bid for Treasury bills, which have accounted for a larger share of government funding in recent years.

Foreign appetite for U.S. debt also appears stronger than headlines may suggest. Treasury auctions continue to reflect confidence, with some longer-dated securities attracting record levels of foreign demand in the second quarter. Banks could provide an increasing source of demand as the regulatory environment evolves. Treasury Secretary Scott Bessent has identified the supplementary leverage ratio (SLR) as a key constraint, suggesting that reforms could lower Treasury yields by 30–70 basis points while improving market functioning. While some SLR reforms were implemented this year, more could occur in the future to improve banks’ demand for Treasuries and market liquidity.

Rethinking Inflation

Despite earlier concerns about the labor market, Fed officials have turned their focus back to inflation as recent data shows prices still running above target, while payroll growth has re-accelerated. Inflation began to gain momentum last year as tariffs filtered through the economy and rose higher following the disruption of energy markets caused by the closure of the Strait of Hormuz.

During his Senate confirmation hearing, Warsh pointed to AI as a potentially disinflationary force, arguing that innovation and productivity gains could help ease price pressures. In the near term, however, the AI buildout has exacerbated inflationary pressures, with demand outstripping supply. He has also suggested reevaluating the inflation measures emphasized by the Fed, expressing a preference for trimmed mean inflation, which filters out extreme price movements to better capture underlying trends.

That approach carries risk. Trimmed mean measures understated inflation during the 2021 surge because they excluded too many large price increases. If today's inflation pressures prove temporary, trimmed measures may offer a cleaner signal and help policymakers avoid overreacting to short-term volatility. However, if inflation remains persistent, relying too heavily on them could leave the Fed behind the curve.

For investors, the more important question is how the Fed interprets incoming data. In the months ahead, we will watch whether the Fed looks through short-term price moves as temporary distortions or treats them as evidence of sustained inflation. Warsh has said he believes price stability is achieved when inflation is low enough that no one talks about it—a standard the Fed has clearly missed in recent years.

At Warsh’s first press conference as chairman, he provided a preview of his priorities by announcing the formation of five task forces focused on the Fed’s communications, balance sheet, data sources, productivity and labor markets, and inflation framework. The announcement suggests an institution in transition, actively rethinking its core practices and likely breaking from the operating approach of recent regimes. The task forces are expected to conclude their work by year-end.

Warsh’s agenda would mark a meaningful shift for the Fed, emphasizing a smaller role, a narrower mandate, and less intervention. Still, meaningful change will require broader support from fellow policymakers, and as Warsh steps into the role, he may find himself reassessing parts of his approach—both to build consensus and in response to the pull of entrenched institutional norms.

Looking Ahead: Inflation, Trade, and the Consumer

Tariffs and Trade

Tariff policy has faded from the headlines this year amid the war in Iran, but attention may return to trade as tensions in the Middle East ease. Earlier this year, the Supreme Court struck down the administration’s use of emergency powers to impose broad tariffs. More than $160 billion in tariffs is now eligible for refunds. The broader direction of U.S. trade policy remains largely unchanged, and trade tensions could re-emerge in the second half of the year as new authorities and negotiations come into focus.

Three relationships remain central: China, the European Union (EU), and the United States–Mexico–Canada Agreement (USMCA). In May, President Trump visited President Xi in China, marking their first meeting since reaching a trade truce last October. Although the summit produced few concrete results, the leaders did establish a new Board of Trade aimed at lowering tariffs and preserving bilateral dialogue. The EU, meanwhile, formally codified its trade framework with the U.S. nearly a year after the agreement was reached. Under the final terms, U.S. imports from the EU will face a 15% tariff, while the EU will eliminate tariffs on U.S. industrial goods and expand preferential access for U.S. agricultural and seafood exports. Formal review of USMCA began on July 1, as tensions remain elevated between the U.S. and its two largest trading partners. Despite signing the agreement in his first term, Trump is now pushing for stricter rules and has threatened withdrawal. While failure to renew would not immediately terminate the pact, it would trigger annual reviews and remain in force through 2036, preserving exemptions for compliant goods. Still, uncertainty could disrupt supply chains and delay investment by reducing long-term visibility. Any member can withdraw from USMCA with six months’ written notice.

Encouragingly, Canada and Mexico have expressed support for extending the agreement and openness to revisions, while key U.S. industry groups have encouraged an extension. Despite lingering uncertainty, we expect leaders to eventually renew the USMCA to preserve the significant economic benefits it provides all three countries.

Peace on the Horizon?

The memorandum of understanding between the United States and Iran marks an important step toward a more durable resolution. Assuming the ceasefire holds, global energy markets may take time to normalize, and we cannot dismiss the risk of renewed tensions. Even so, the recent decline in oil prices suggests that markets believe the conflict is nearing its end. As a result, headline inflation should ease gradually in the months ahead.

Price Pressures Still Present

In May, the consumer price inflation rose to 4.2% year over year, its highest level in three years. Producer prices climbed 6.4%, the highest since 2022, driven in large part by an almost 11% increase in energy costs.

While easing oil prices should help moderate some of these pressures in the months ahead, inflation is likely to remain elevated in the near term. Beyond energy and tariffs, structural demand tied to the ongoing AI buildout is creating additional price pressures. Strong demand for semiconductors has contributed to supply constraints across portions of the technology supply chain, pushing input costs higher. In June, several firms announced price increases, including Apple, raised prices on Macbooks and iPads, and Microsoft, which announced higher prices for its Xbox lineup.

Taken together, higher energy costs, lingering tariff effects, and the ongoing AI buildout—alongside a still-resilient labor market—make a near-term rate cut unlikely. Although markets are pricing in additional hikes and roughly half of Fed officials expect further tightening this year, we think easing tensions in the Middle East and stable inflation expectations may give the Fed sufficient justification to remain on hold.

Checking in on the Consumer

Recent corporate earnings calls tell a familiar story: consumer spending remains resilient despite signs of moderation among lower-income households. Elevated asset prices and a strong tax refund season helped cushion the impact of higher energy costs as households drew down savings. Easing gas prices should also provide gradual relief in the second half of the year. However, income growth has softened. Real disposable income has been pressured by higher inflation and slower wage growth, while slower immigration has also tempered overall income growth. The boost from tax refunds will quickly fade as the year progresses, adding pressure to already constrained real incomes. Even so, household wealth remains at record highs and debt service ratios remain below pre-pandemic levels.

The labor market regained traction in the first half of the year, alleviating downside employment concerns. Through May, job growth has averaged 113,000 per month, up from an average decline of 8,000 in the second half of 2025. Tepid jobless claims and a still-low layoff rate are also encouraging. Together, resilient consumer spending and a firmer labor market have shifted policymakers’ focus back to inflation, reducing the likelihood of near-term rate cuts and raising the prospect of further tightening.

Conclusion: Navigating an Uncertain Second Half

The second quarter underscored the crosscurrents shaping today's economy. While equity markets rallied, corporate earnings remained strong, and geopolitical tensions began to ease, inflation stayed above target, and the outlook for interest rates became less certain. At the same time, the transition to a new Fed chair introduces the potential for a meaningful shift in how monetary policy is communicated and implemented.

Although easing tensions in the Middle East should gradually reduce energy-related inflation, lingering tariff effects, AI-driven investment demand, and a resilient labor market suggest price pressures will not fade quickly. In this environment, we believe investors are best served by maintaining a disciplined, long-term approach rather than reacting to short-term headlines. While the policy backdrop may evolve under the new Fed leadership, a diversified portfolio remains the most effective way to navigate uncertainty and participate in future opportunities.

Market Recap

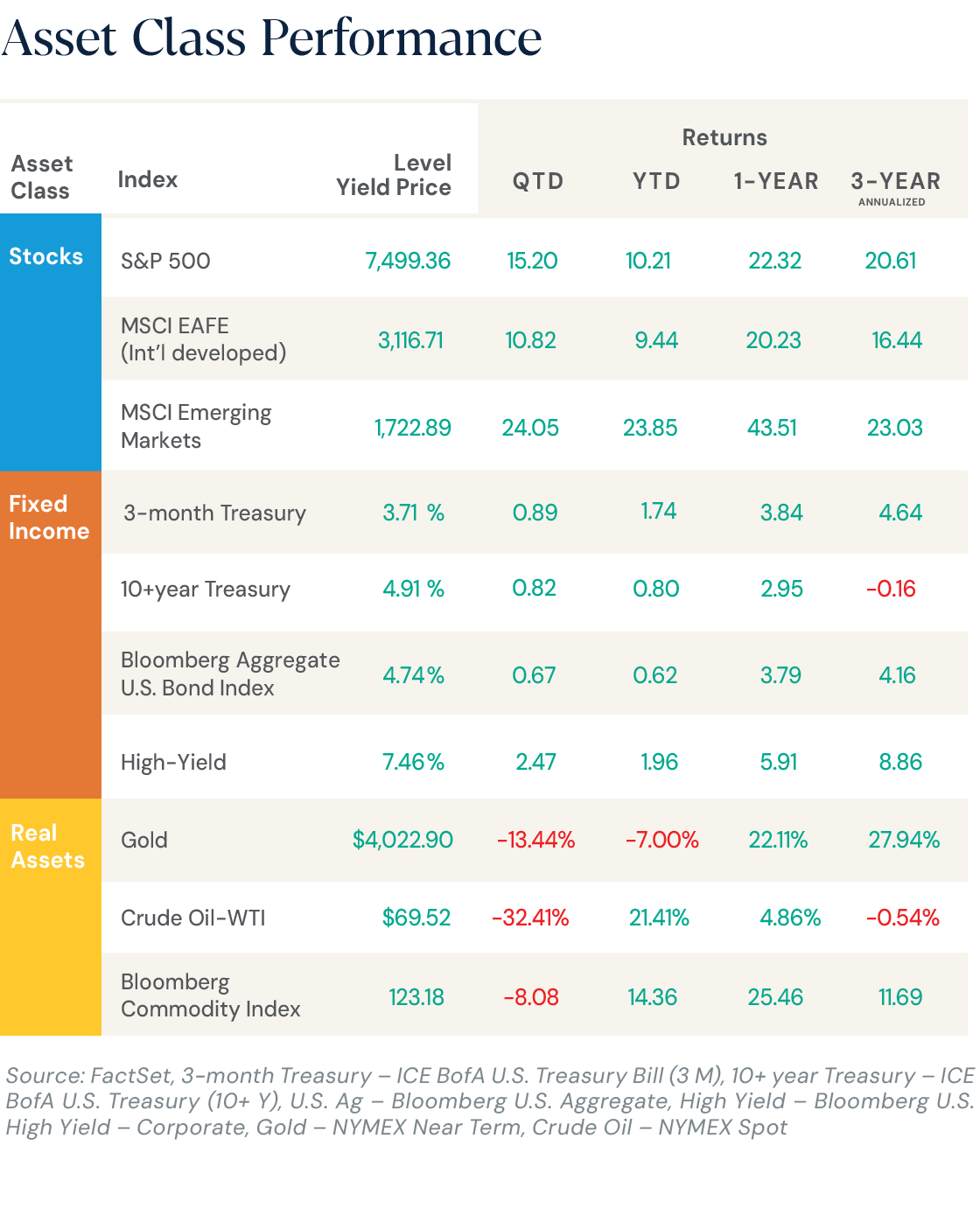

The second quarter began with a ceasefire in Iran that sent stocks marching higher for most of the quarter before running into some turbulence as markets digested news of the SpaceX IPO. The labor market showed renewed strength during the quarter, and firm inflation continues to drive market expectations of a rate hike before year-end. Emerging market equities outperformed others during the quarter, rising 24%, while developed international stocks increased nearly 11%. U.S. equities also posted strong gains, with the S&P 500 finishing up 15% after falling 4% to start the year.

Gold took a breather during the quarter, sliding 14%. Commodities rose during the quarter before retreating after the U.S. and Iran reached a memorandum of understanding, ultimately finishing the quarter down 8%. Bond markets were essentially flat, rising less than 1%.

S&P 500 companies posted first-quarter earnings growth of 28.6%, the strongest since the fourth quarter of 2021, with 85% of companies exceeding analysts’ expectations―the highest share since 2021. Although earnings growth was robust, results were partially boosted by one-time gains at several large companies. Even so, all 11 sectors exceeded expectations, led by Information Technology with 54% earnings growth. Analysts now expect earnings growth of 24% in 2026, up from 13% at the start of the year. Looking ahead to 2027, earnings are projected to grow more than 16%.

expectations,led by Information Technology with 54% earnings growth. Analysts now expect earningsgrowth of 24% in 2026, up from 13% at the start of the year. Looking ahead to2027, earnings are projected to grow more than 16%.

As with any investment strategy, there is potential for profit as well as the possibility of loss. Blue Trust does not guarantee any minimum level of investment performance or the success of any investment strategy. All investments involve risk and investment recommendations will not always be profitable. Diversification does not guarantee investment returns and does not eliminate loss. Past performance does not guarantee future results.

Private funds are speculative investments and are not suitable for all investors, nor do they represent a complete investment program. Private funds are available only to qualified investors who are comfortable with the substantial risks associated with investing in private funds. An investment in a private fund includes the risks inherent in an investment in securities.

CAS00002892-06-26

1 Jay Ritter, University of Florida https://site.warrington.ufl.edu/ritter/files/IPO-Statistics.pdf

Looking for personalized guidance?

Our advisors bring financial expertise and biblical wisdom together to guide the decisions shaping your future.