SpaceX, Anthropic, and OpenAI are among the most talked-about companies in the world, and the chance to buy into their public debuts is generating real excitement. But excitement isn't a strategy. In this piece, we look at what these offerings actually are, who can realistically buy in at the IPO price, and what history says about how IPOs tend to perform.

Few investment stories capture the public imagination like rockets and artificial intelligence. SpaceX, Anthropic, and OpenAI are not typical initial public offering (IPO) candidates. They are well-known private companies, each valued at roughly $1 trillion or more, operating in markets that many investors believe could shape the next decade of economic growth.

We'll look beyond the headlines to explain access, valuation, historical IPO performance, and how investors can approach these potential mega-IPOs with discipline.

These companies may be worth owning someday, but clients should exercise caution: avoid chasing IPO access, scrutinize valuations, and restrict position sizes to a satellite holding.

What these companies are and why the market cares

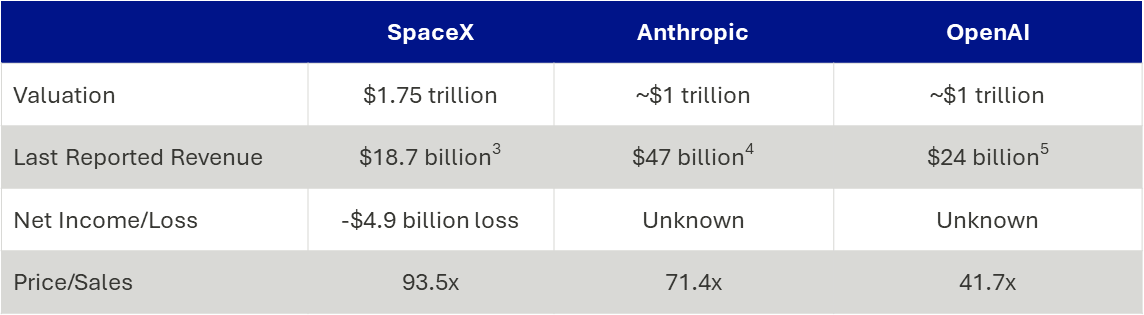

SpaceX is best known for rocket launches, Starlink satellite internet, and broader space infrastructure, and now AI through its merger with xAI. Its potential IPO is especially notable because it could be one of the largest public offerings ever, with a proposed $75 billion capital raise at a roughly $1.75 trillion valuation.

Anthropic is an artificial intelligence company best known for Claude. Anthropic announced on June 1, 2026, that it had confidentially submitted a draft IPO registration statement, though the company said the number of shares and price range had not yet been determined. Anthropic recently raised $65 billion in May 2026, valuing the company at $965 billion.1

OpenAI is the company behind ChatGPT and one of the leading developers of large language models. On June 8, 2026, OpenAI also confidentially filed for an IPO, so the number of shares and price range remain undetermined. OpenAI recently raised $122 billion in March 2026 bringing its value to $852 billion.2

Investors are watching closely because these companies sit at the intersection of several powerful themes: artificial intelligence, cloud infrastructure, satellite connectivity, defense technology, and the long-term commercialization of space, but the scale of the opportunity also means the scale of expectations is extremely high.

Who gets access?

Access is one of the most misunderstood parts of IPO investing.

Before IPO, ownership is generally limited to founders, employees, venture capital funds, private equity investors, sovereign wealth funds, large institutions, and certain private secondary market participants. After the IPO, access broadens, but not everyone gets access at the IPO price.

The SEC notes that the company and its underwriters control IPO share allocations, and smaller investors may find it difficult to receive shares at the IPO price.

Most retail investors typically gain exposure in one of three ways: buying shares after trading begins, owning an active mutual fund or ETF that buys shares, or owning a passive index fund after the company is eventually added to an index.

SpaceX is an exception. SpaceX is targeting allocating 30% of its offering to individual investors and brokerage firms: Fidelity, Charles Schwab, Robinhood, SoFi, and E*TRADE have received some sort of allocation. These firms have various protocols for distributing shares, so having an account does not guarantee access.

There are publicly traded funds that claim to have exposure to some of these private companies. While that can be true, we would urge caution and to read the fine print. Some funds’ actual exposure may be as little as ~1%, often held indirectly through special purpose vehicles (SPVs) rather than direct ownership. Anthropic recently announced they won’t recognize any shareholders who aren’t approved by their board, and OpenAI has shared similar statements, so the status of these SPVs’ ownership is uncertain.

Just because you can, does it mean you should?

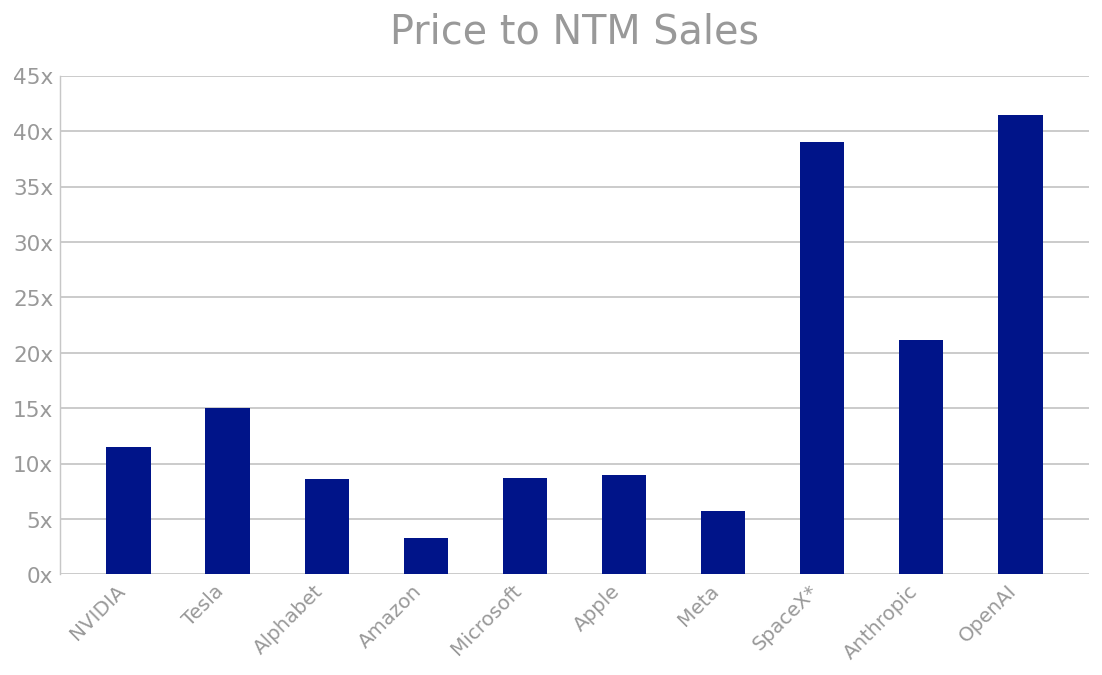

What are these companies’ worth? That is the key question. The answer is subjective. By traditional metrics such as price-to-sales, these companies look expensive relative to established peers.

Numbers are likely outdated and speculative as these are private companies and SpaceX is the only company to have filed a public S-1. SpaceX reported $18.7 billion revenue when filing their S-1. Since filing, SpaceX has announced two massive compute leasing deals with Anthropic for $15 billion/year and Google for $11 billion/year. It is important to note that these contracts can be cancelled at any time by either party.

NTM = next-twelve-month sales which better reflects revenue for SpaceX, Anthropic, and Open AI as their revenue has been reported as an “annual recurring revenue” figure. SpaceX* includes recent compute deals with Anthropic and Google.

Source for NVIDIA, Tesla, Alphabet, Amazon, Microsoft, Apple, and Meta (M7) Price/Sales: FactSet as of 5/31/26

Investors who buy these companies at the IPO are generally making one of two assumptions: either a) they are attempting to trade the stock based on momentum and sentiment or b) believe these companies will grow significantly more than expectations to justify these high valuations.

What history says about IPO returns

IPO investing can be exciting, but the historical record is mixed.

University of Florida professor Jay Ritter’s long-running IPO data6 show that from 2001 through 2024, U.S. IPOs had an average first-day return of 21.7%a but the average three-year market-adjusted return was negative 18.9%. In other words, IPOs have often produced a strong first-day “pop,” but many have underperformed over longer periods.

Ritter’s broader 1980–2024 data also show that IPOs returned an average of 4.9% in the first six months and 5.6% over the first year, compared with 11.4% for size-matched public companies over the first year.

A separate Nasdaq analysis of 2010–2020 IPOs found that nearly two-thirds of IPOs underperformed the market three years after going public.7

For a more recent “mega tech IPO” lens, one Truist sample of 30 major IPOs reported average returns of 4% after one month, 20% after three months, 1% after six months, and 14% after twelve months. But the median twelve-month return was negative 9%, and the average maximum first-year drawdown was 55%.8

The takeaway: IPO outcomes are highly skewed. A few big winners can lift the average, while many individual IPOs disappoint.

Key risks and potential rewards

The potential rewards are easy to understand. These companies have large markets, strong brands, sophisticated technology, and scarcity value. There are not many public companies with direct exposure to private space infrastructure, frontier AI models, and massive compute demand.

But the risks are equally important.

First, valuation matters. These mega IPOs are set to trade at significant premiums compared to existing peers.

Second, some of these companies are still highly capital intensive. AI infrastructure requires enormous spending on chips, data centers, energy, engineering talent, and model development. Space infrastructure requires repeated technical execution, regulatory approvals, and major capital investment.

Third, early trading can be volatile. IPOs often involve limited float, lockup periods, heavy media attention, and rapid changes in investor sentiment.

Don’t forget about passive ownership

Many clients may eventually own these companies even if they never buy shares directly. S&P has stated it won’t fast-track SpaceX into the S&P 500, but some index rules are changing. Schwab has noted that index providers have been considering or adopting faster inclusion rules for very large IPOs. Nasdaq-100 rules now allow certain large IPOs to be added after as few as 15 trading days if they meet size and eligibility requirements. Russell will allow it in as few as five days.

After some initial analysis, it does not appear that SpaceX will have a material (>2% weight) presence in some of the traditional indexes like the Nasdaq. Still, for some individuals, this passive exposure will be enough. Therefore, the relevant question may not be, “Should I buy SpaceX, Anthropic, or OpenAI on day one?” It may be, “Should I wait knowing I will eventually have exposure through my diversified stock funds if these companies enter major indexes?”

How clients should think about sizing and patience

A prudent approach begins with the financial plan, not the headline.

For most clients, any single IPO should be considered a satellite position, not a core holding. The core of a portfolio should remain diversified across time frames, asset classes, geographies, sectors, and investment styles.

Before buying, investors should ask:

1. How much exposure do I already have to technology, AI, and growth stocks?

2. Would I be comfortable if the stock fell 30%, 40%, or 50% in the first year?

3. Am I buying because the valuation is attractive, or because the story is exciting?

4. Does this investment fit my long-term plan, or is it driven by fear of missing out?

5. At what price would I sell this investment?

There may be good reasons to own these companies over time, but patience matters. IPOs often trade with limited information, intense enthusiasm, and high expectations. Waiting for public reporting, earnings history, index inclusion dynamics, and post-lockup trading can sometimes provide a clearer picture.

For Blue Trust clients, the goal is not to avoid innovation. The goal is to pursue opportunities with wisdom, discipline, and an appropriate understanding of risk.

Sources

1 https://www.anthropic.com/news/series-h

2 https://techcrunch.com/2026/03/31/openai-not-yet-public-raises-3b-from-retail-investors-in-monster-122b-fund-raise/

3 SpaceX S-1, https://www.reuters.com/business/media-telecom/spacex-signs-cloud-deal-with-google-2026-06-05/

4 https://www.anthropic.com/news/series-h

5 https://openai.com/index/accelerating-the-next-phase-ai/

6 Initial Public Offerings: Updated Statistics Jay R. Ritter Eugene F. Brigham Department of Finance, Insurance, and Real Estate Warrington College of Business, University of Florida

7 htps://www.nasdaq.com/articles/what-happens-to-ipos-over-the-long-run-2021-04-15

8 https://www.morningstar.com/news/marketwatch/20260603137/looking-to-buy-into-the-spacex-ipo-this-scary-chart-might-make-you-think-twice

__

a The average first-day return is calculated as the percentage change from the official offer price to the closing market price at the end of the first day of public trading.

Looking for personalized guidance?

Our advisors bring financial expertise and biblical wisdom together to guide the decisions shaping your future.