Is the U.S. Dollar’s Status in Jeopardy?

Questioning if the U.S. dollar’s future as the world’s reserve currency is in jeopardy isn’t new, but it’s emerged again lately amid headlines relating to foreign governments trading in non-U.S. dollars, central banks diversifying currency reserves in the wake of the “weaponization” of the financial system against Russia, and the U.S.’s growing debt. In this blog, we discuss what a world reserve currency is and why we believe it is unlikely the U.S. dollar will lose its status in the near future.

What is a reserve currency?

A world reserve currency is a medium of exchange that is widely held by governments and institutions as part of their foreign exchange reserves. These currencies are used to facilitate international trade, investment, and financial transactions. A good reserve currency must be stable, liquid, widely accepted, and associated with a large and robust economy that is backed by trusted institutions and characterized by political stability. The U.S. dollar has historically met these criteria, which is one reason why it has been the dominant world reserve currency for much of the past century.

The U.S. dollar isn’t the only reserve currency. The International Monetary Fund (IMF), the body responsible for monitoring the international monetary system, recognizes eight major reserve currencies: the Australian dollar, the British pound sterling, the Canadian dollar, the Chinese renminbi, the euro, the Japanese yen, the Swiss franc, and the U.S. dollar. The U.S. dollar is by far the most-held reserve currency, making up more than 60 percent of global foreign exchange reserves.

What are the benefits of a reserve currency?

The use of a world reserve currency can confer significant benefits, including:

- Greater liquidity: World reserve currencies are widely held by governments and institutions around the world, which creates a deep and liquid market for the currency, making it easier for buyers and sellers to transact with each other.

- Reduced exchange-rate risk: When world reserve currencies are used in international trade and finance, there is a reduced need for businesses and investors to hedge against exchange-rate fluctuations, which can lower transaction costs and reduce overall risk.

- Easier access to credit: Countries with reserve currencies often enjoy lower borrowing costs as lenders view them as safer and more stable than other countries. This position can make it easier for governments and businesses to access credit, which can in turn stimulate economic growth.

- Safe-haven status: During periods of economic stress, investors often exit risky investments and typically invest in U.S. dollar-based cash and government securities.

History of dominant reserve currencies

While several reserve currencies can coexist, there is usually one that becomes the world’s dominant medium. Several different currencies have held this status throughout history. The dominant reserve currency was the Venetian ducat from the 13th‒17th centuries, the Spanish real in the 16th‒19th centuries, the Dutch guilder also in the 17th‒18th centuries, the British pound sterling in the 19th‒20th centuries, and the U.S. dollar since World War II and the Bretton Woods agreement in 1944. The French franc, German mark, and Japanese yen all briefly emerged as potential candidates for a dominant world reserve currency, but ultimately were surpassed due to political and/or economic events.

Concerns with the U.S. Dollar

Once a currency becomes the dominant world reserve currency, it usually reigns for an extended period because it becomes entrenched in the financial system and is quite difficult to supplant. Because no earthly government will last forever, we acknowledge that the U.S. dollar could lose its status as the world’s reserve currency, but here are some reasons why it’s more difficult than one might think and why we’re not expecting it to happen, at least in the near future.

- The size and stability of the U.S. economy. The U.S. is the world’s largest economy, with Gross Domestic Product (GDP) of over $25 trillion in 2022,[1] which accounts for over 20% of the world’s GDP.

- The liquidity of U.S. financial markets. The U.S. stock market is the largest in the world by market capitalization, and the U.S. bond market is the largest in the world by value.[2] The U.S. dollar is also the most traded currency in the world, with around 88% of all foreign exchange transactions involving the U.S. dollar.[3]

- The dominance of the U.S. in international trade. The U.S. is the world’s second-largest exporter and importer of goods.[4] The U.S. dollar is also the dominant currency used in international trade, with around 40%-50% of all global trade settled in U.S. dollars.[5]

- The network effects of the U.S. dollar. The U.S. dollar is widely used and accepted around the world. Around 60% of all foreign exchange reserves held by central banks are denominated in U.S. dollars and commodities worldwide are typically priced in U.S. dollars.[6]

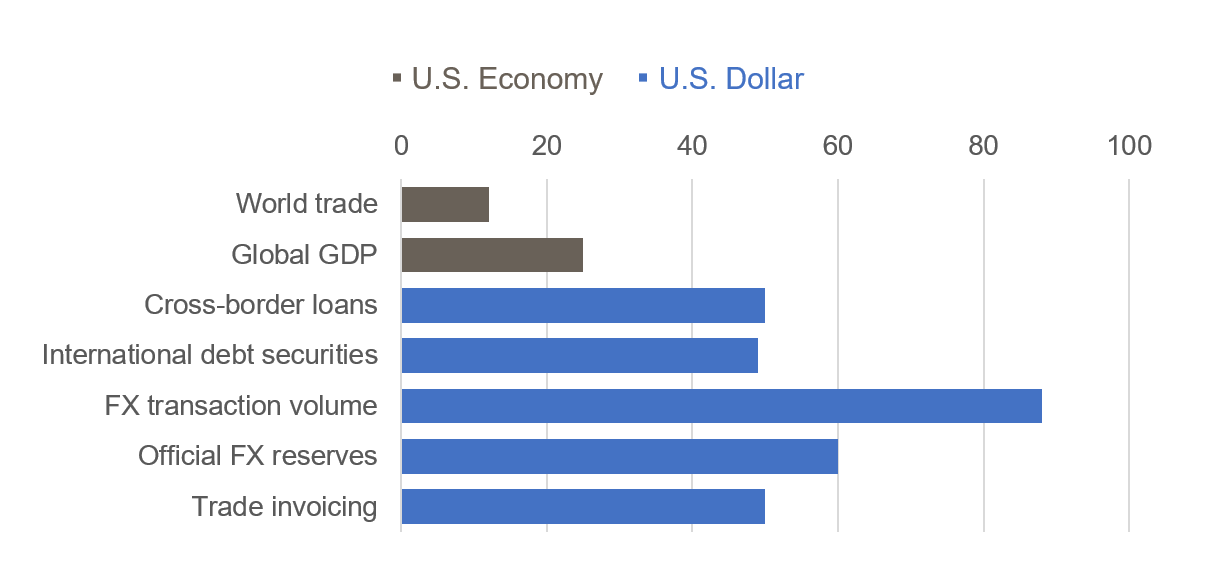

The U.S. dollar’s role in the international monetary system eclipses the U.S.’s presence in the global economy as summarized in the chart below.

U.S. Economy and Dollar Share of Global Markets (%)

Source: G Gopinath, “The international price system”, NBER Working Papers, no 2164, 2015; IMF; Bloomberg; CPB World Trade Monitor; BIS debt securities; BIS locational banking statistics; BIS triennial Central Bank Survey. As shown on https://www.bis.org/publ/qtrpdf/r_qt2212x.htm

For years, there has been growing interest by some countries to settle international trade in non-dollar currencies. This desire is something we expect to continue in a gradual fashion—not something that will occur in a sudden shift. It’s logical that countries would want to diversify their foreign currency exposure, whether in terms of foreign trade or foreign reserves, especially as the U.S. slowly shrinks as a percentage of global GDP, trade, etc. However, it’s important to remember that the U.S. dollar is the most liquid, widely accepted, and stable currency. It is supported by a dominant military, deep financial system, steady legal system, and the large competitive economy of the U.S. Therefore, we believe the U.S. dollar will continue to maintain its global reserve status for the foreseeable future, as there is no other single currency that is currently superior.

With that said, we do not view the gradual diversification away from the U.S. dollar as the dominant global reserve currency as cause for concern, rather a natural evolution. Consider Britain; the dollar’s rise did not result in the demise of Britain. Other countries, like Japan and China, have also grown even though their currencies are not dominant. The Chinese renminbi (or yuan) is perhaps the leading contender to eventually overtake the U.S. dollar, but it still has a ways to go. Chinese GDP already exceeds U.S. GDP by 18% on a purchasing power parity basis[7] and is projected to exceed U.S. GDP in nominal terms in the 2030s. However, their currency is still lagging the U.S. substantially in some key metrics and attributes, including:

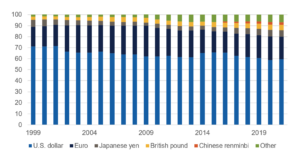

- Store of value/foreign exchange reserves. A key function of a currency is store of value, which means the currency can be saved and retrieved in the future without a significant loss of purchasing power. One measure of confidence in a currency as a store of value is its usage in official foreign exchange reserves. As shown in Figure 2, the dollar comprised 60% of globally disclosed official foreign reserves in 2021 while the Chinese renminbi only accounted for 2%.

Foreign Exchange Reserves

Figure 2

Source: IMF COFER. Share of globally disclosed foreign exchange reserves. At current exchange rates. Data are annual and extend from 1999 through 2021. 2021 is 2021-Q1. Chinese renminbi is 0 until 2015-Q2. As shown on www.federalreserve.gov/econres/notes/feds-notes/the-international-role-of-the-u-s-dollar-20211006.html#fig2

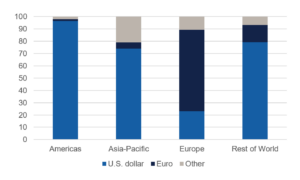

- Medium of exchange. A currency’s usage as a medium of exchange can also measure its international prominence. As shown in Figure 3, the U.S. dollar is overwhelmingly the world’s most frequently used currency in global trade, while other currencies, including the renminbi, comprise a small portion.

Share of Export Invoicing

Figure 3

Source: IMF Direction of Trade; Central Bank of the Republic of China; Boz et al. (2020); Board staff calculations. Average annual currency composition of export invoicing, where data are available. Data extend from 1999 through 2019. Regions are those defined by the IMF. As shown on www.federalreserve.gov/econres/notes/feds-notes/the-international-role-of-the-u-s-dollar-20211006.html#fig2

- Currency convertibility/freely exchangeable. A convertible currency is a legal tender that can be easily bought or sold on the foreign exchange market with little to no restrictions. The U.S. has a convertible currency, but the Chinese renminbi does not as China restricts such conversions and manipulates the value of its currency.

Investment Implications

We believe the dollar is currently overvalued from a purchasing-power perspective, and that’s one of the reasons that we think international equities are currently more attractive than U.S. equities. The potential migration of the world’s reserve currency away from the dollar is another reason we support international diversification. However, seeking to invest in the world’s next dominant reserve currency is not a fundamental principle of our investment philosophy. The U.S. gained its status as the world’s dominant currency because it promoted human productivity and economic freedom, two of Blue Trust’s core principles. These principles help guide our investment selection as we look to diversify internationally in countries that promote these same principles.

Our investment team and advisors will continue to closely monitor the U.S. dollar and make portfolio adjustments as needed. If you have additional questions, please reach out to your Blue Trust advisor or contact us at 800.987.2987 or email blog@bluetrust.com.

[1] source: Bureau of Economic Analysis

[2] Source: World Federation of Exchanges and the Securities Industry and Financial Markets Association (SIFMA)

[3] Source: Bank for International Settlements

[4] Source: World Trade Organization

[5] Source: Bank for International Settlements

[6] ibid

[7] Source: IMF World Economic Outlook, April 2023