Supercore Inflation: The New Focus of the Federal Reserve

The Federal Reserve (Fed) has been raising interest rates for a year in its attempt to cool inflation; but with inflation still hovering above 6%,1 it remains far from the Fed’s 2% target. At first glance, it appears the Fed has a lot left to do, but the Fed believes there’s only one major inflation component still of concern—supercore inflation.

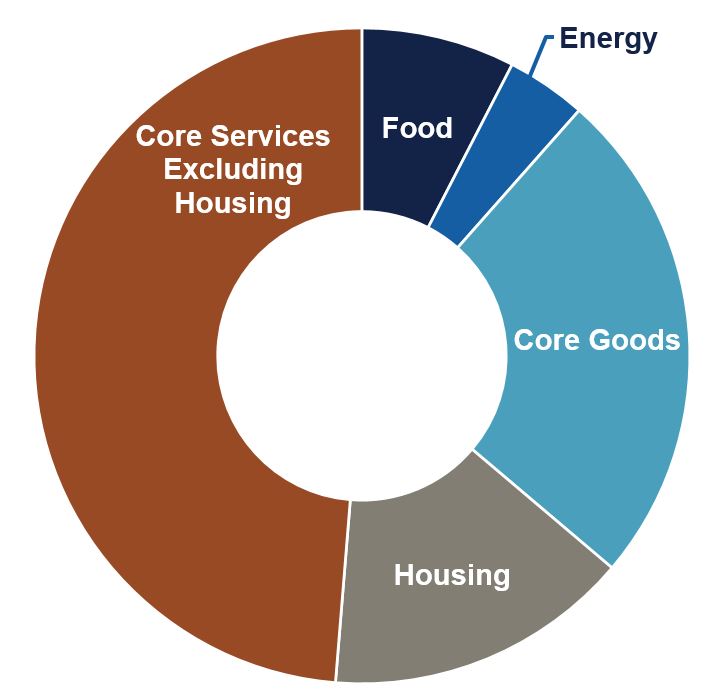

While the Fed’s preferred measure of inflation (known as core inflation) excludes food and energy, due to their high volatility, the Fed has recently begun to narrow its focus even further. Specifically, the Fed has dissected core inflation into three components: core goods, housing, and core services excluding housing. Because this last component is viewed as the centerpiece of core inflation, it’s often called “supercore.”

Consumer Spending Categories

Source: Bureau of Economic Analysis. Based on 2021 personal consumption expenditures.

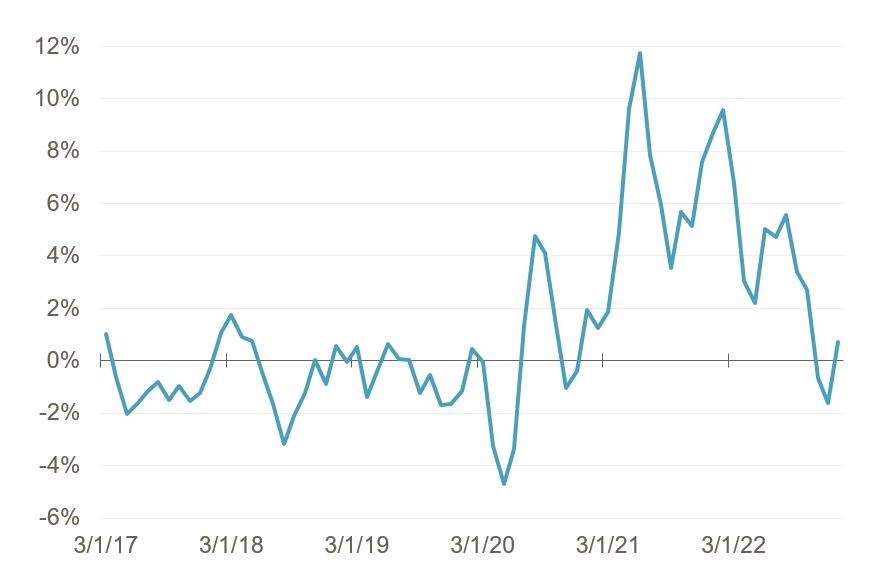

The Fed is now deemphasizing core goods (e.g., vehicles, furniture, etc.) in their analysis of inflation because prices of these products have stabilized. As consumer spending shifted from goods back to services and supply chain pressures eased, inflation of core goods has reverted to pre-COVID levels, as shown below.

Core Goods Inflation

(3-Month Annualized Change)

Source: Bureau of Economic Analysis. Data is through January 2023.

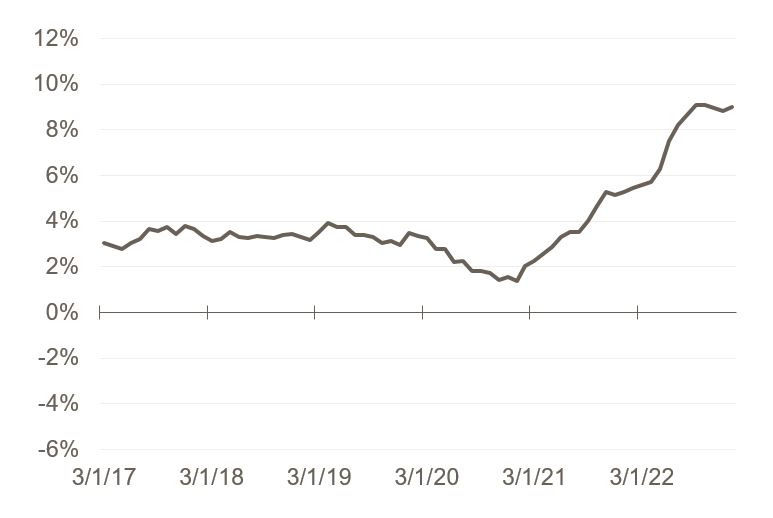

Housing, on the other hand, is still experiencing very high inflation (see chart below). However, the Fed expects housing inflation to begin receding this summer. There is strong evidence, based on recent price declines of new leases, that rent inflation will cool significantly this summer, as prices of existing leases (which typically renew annually) catch up to current rental prices. Thus, the Fed is not concerned about high inflation continuing in housing.2

Housing Inflation

(3-Month Annualized Change)

Source: Bureau of Economic Analysis. Data is through January 2023.

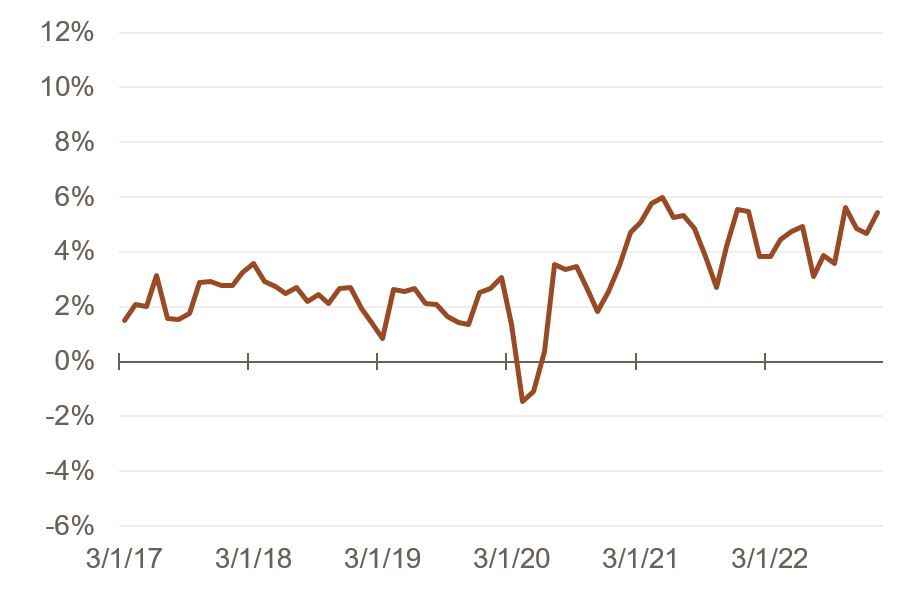

After excluding core goods and housing, what’s left is a range of services like healthcare, restaurants, and education, which are referred to as core services excluding housing. Pre-COVID, inflation in this sector averaged a little more than 2%. Post-COVID, it’s been consistently above 4%, and shown no evidence of cooling (see chart below).

Core Services Excluding Housing Inflation

(3-Month Annualized Change)

Source: Bureau of Economic Analysis. Data is through January 2023.

The Fed believes the key to cooling supercore inflation is a weaker labor market because employee compensation is the main cost to businesses providing these services. However, the labor market has shown little signs of cooling. Almost every indicator (e.g., the unemployment rate, change in payrolls, and the number of job openings) exhibits strength. So, what could soften the labor market?

The Fed would welcome an increase in the supply of labor (e.g., from increased legal immigration or participation from the existing population), but it’s neither something they can influence nor expect to occur. A jump in labor productivity would also help, but the Fed cannot affect or rely upon it either. Instead, the Fed must use higher interest rates to weaken the demand for labor. However, this inflation cure will likely inflict economic pain via reduced consumer spending, lower profit margins, and eventually higher layoffs.

While it’s possible that labor demand could soften without a material increase in layoffs (e.g., by a sharp decline in job openings), it is unlikely. In fact, the Fed projects that unemployment will rise by 0.9% this year, which would be historically consistent with the start of a recession.3 So far though, consumer spending and corporate profits have remained resilient, and layoffs have stayed subdued. In the short-term, this trend is positive as it signals that an imminent recession is unlikely. However, while inflation remains high, investors will likely view economic strength negatively. Because the economy is still far from equilibrium, there is increased risk that the Fed will need to keep rates higher, and for longer, than many experts anticipated just a few months ago. More restrictive monetary policy could result in a sharper or longer downturn in the future, leading us to believe that now is not the time to take undue risk with money needed in the short- and intermediate-term. However, bumps along the way could provide attractive long-term investment opportunities.

Our investment team and advisors will continue to closely monitor the markets, inflation, and the economy and make portfolio adjustments as needed. If you have additional questions, please reach out to your Blue Trust advisor or contact us at 800.987.2987 or email blog@bluetrust.com.