The State of U.S. Commercial Real Estate: Risks and Opportunities

Bank failures have put stress on the markets this year, but another area that has the potential to frustrate the economy is the $20 trillion commercial real estate (CRE) market. Commercial real estate is a broad term that encompasses various types of properties used for business purposes, such as offices, retail shops, industrial and logistics warehouses, multifamily housing facilities, and hospitality establishments.

CRE is a vital sector of the economy, as it provides space for businesses to operate, generate income, and create jobs. However, CRE is also a complex and dynamic market influenced by many factors, such as macroeconomic conditions, consumer preferences, technological innovations, demographic shifts, and environmental issues. These factors can affect the supply and demand of different types of properties, as well as their values and performance.

In this article, we will examine the current state of the U.S. CRE market, highlighting the key trends and challenges shaping its outlook. We will also review the role and risks of banks in the CRE market, especially for office and retail properties hit hard by the pandemic and its aftermath.

The Health of the Commercial Real Estate Market

CRE is a large sector that varies significantly depending on the local market. The current assessment of the CRE market is complicated as some sectors, such as multifamily and industrial, have prospered, and others, such as office and retail, have struggled. For simplicity, in this article we will focus on four of the main property sectors: Office, Apartments (Multifamily), Industrial, and Retail.

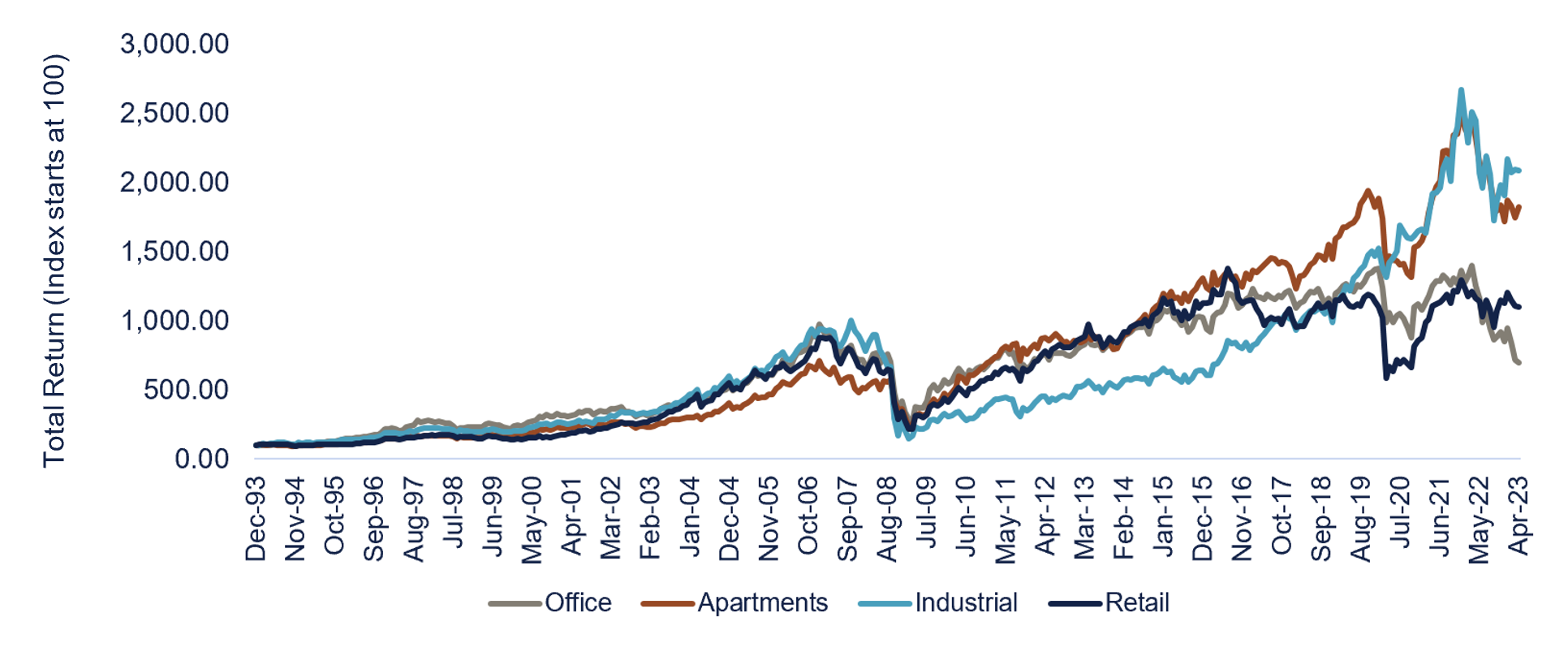

Total Return of CRE by Property Sector

Source: Nareit. Total return of U.S. Real Estate Index’s from December 1993 – April 2023

Multifamily and Industrial Properties: Strong

In recent years, multifamily and industrial properties were the highest-performing asset classes among CRE properties. These segments benefited from strong demand, limited supply, and favorable demographics and trends.

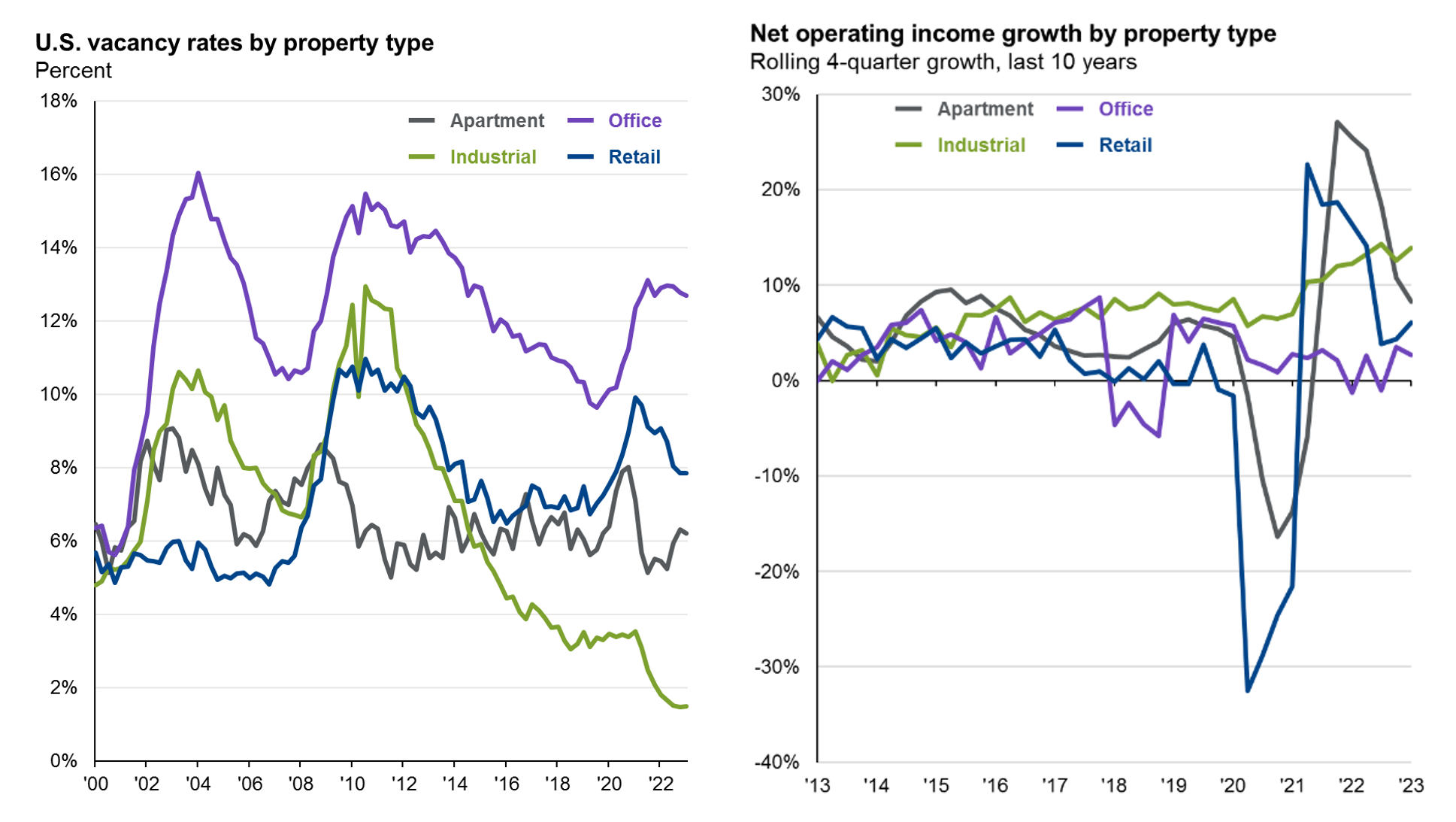

Multifamily properties, which include apartments and condominiums, have been supported by the high cost of homeownership, the growth of urbanization and migration, and the demand for affordable and workforce housing. The vacancy rate for multifamily properties is around 6%, and net operating income (NOI) growth (income after expenses) is about 8% after seeing record highs above 25% during COVID.1

The surge of e-commerce, the expansion of supply chains, the need for last-mile delivery, and the adoption of new technologies have driven up the demand for industrial and logistics properties, which include warehouses, distribution centers, and fulfillment centers. Vacancies for this sector are below 2%, with NOI growth currently around 14%.

The outlook for these two sectors remains strong. However, while multifamily supply and demand are in balance, demand for industrial facilities is higher than the current supply, but many expect both sectors to continue to enjoy favorable trends.

Source: NCREIF, NAREIT, Statista, J.P. Morgan Asset Management. NOI is net operating income. NOI data as of May 31, 2023. Vacancy rate data as of March 31, 2023.

Office and Retail Properties: Under Stress

On the other hand, office and retail properties have faced more challenges and uncertainty in recent years. The pandemic caused a decline in occupancy, utilization, and leasing activity for office properties, which include buildings occupied by businesses, professionals, and government agencies. Many companies have also adopted hybrid work models that allow employees to work partially from home or other locations, reducing their need for office space. Office vacancies spiked during the pandemic and have remained around 13%. NOI growth turned down during the pandemic but has recovered to about 2%.

Retail properties, which include shopping centers, malls, and stores that sell goods and services to consumers, have been affected by the recent rise of e-commerce, the change in consumer behavior, and the closure of many brick-and-mortar retailers. Many consumers have shifted their spending online or to essential and experiential categories, reducing their demand for physical retail space. However, retail has made a slight comeback as excess savings and pent-up demand have increased retail sales. Vacancies are around 8%, and NOI growth, after whipsawing during the pandemic, is around 6%.

The outlook for office and retail properties is unclear, as these segments face continued uncertainty and volatility. However, office properties have potential opportunities with the recovery of employment and economic activity, the adaptation of hybrid work models and flexible office spaces, and the renovation and repositioning of existing buildings. Similarly, transforming shopping centers and malls into mixed-use destinations, integrating e-commerce and omnichannel strategies, expanding experiential and service-oriented categories, and adopting digital and contactless technologies could positively impact retail properties.

The Role and Risks of Banks in the CRE Market

Banks are major players in the CRE market because they provide loans to businesses and investors that acquire, develop, or refinance properties. Banks, especially large ones, are also part of the securitization market, as they typically package their loans into financial products and sell them to investors, allowing banks to raise more money to make new loans.

Bank balance sheets have come under the spotlight recently after the failures of Silicon Valley Bank and First Republic Bank, and regulators are closely scrutinizing CRE loans—especially for office and retail properties that were hit hard by the pandemic. These loans are facing risks from increased interest rates, lower occupancy, and decreased property values (depending on the sector), all of which could affect the repayment and refinancing of their loans, as well as the value and performance of their properties.

Risk of Default and Potential Impacts

The delinquency rate of CRE loans is currently very low, around 0.7%. However, with interest and vacancy rates rising, the number of delinquencies is expected to increase.

If defaults on CRE debt increase, the impact on banks would depend on the magnitude and duration of the defaults, as well as the exposure and resilience of the banks. However, some possible consequences are losses and write-offs on bank balance sheets, regulatory scrutiny, market volatility, and credit contraction and contagion if defaults are significant.

Are CRE loan defaults the next significant financial crisis?

It’s possible, but no one knows for sure. The following data may help assuage concerns about a potential repeat of the 2007‒2009 Global Financial Crisis (GFC).

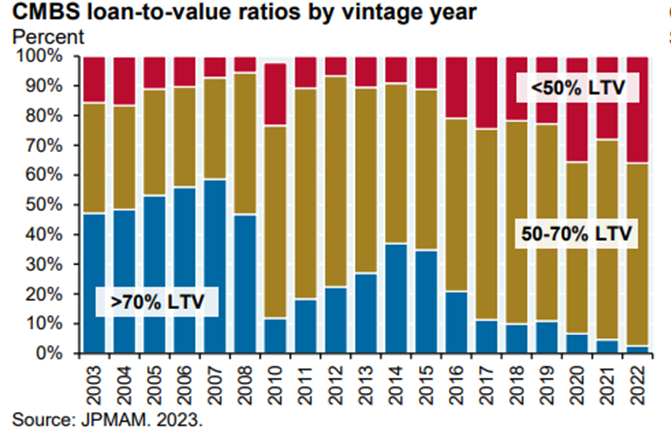

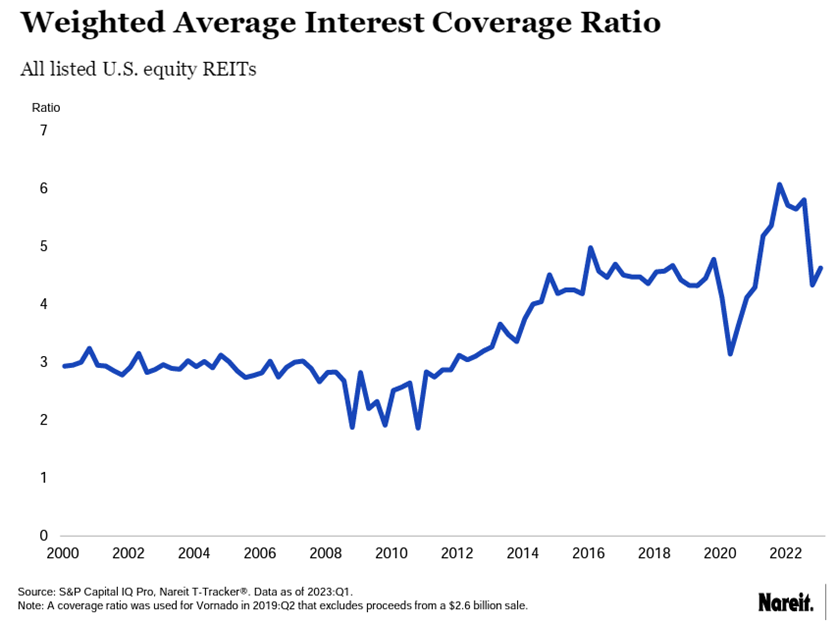

- CRE lending standards are stricter post-GFC. The chart below illustrates how loan-to-value (LTV) ratios have become more conservative, and the second chart shows how debt service coverage ratios have improved.

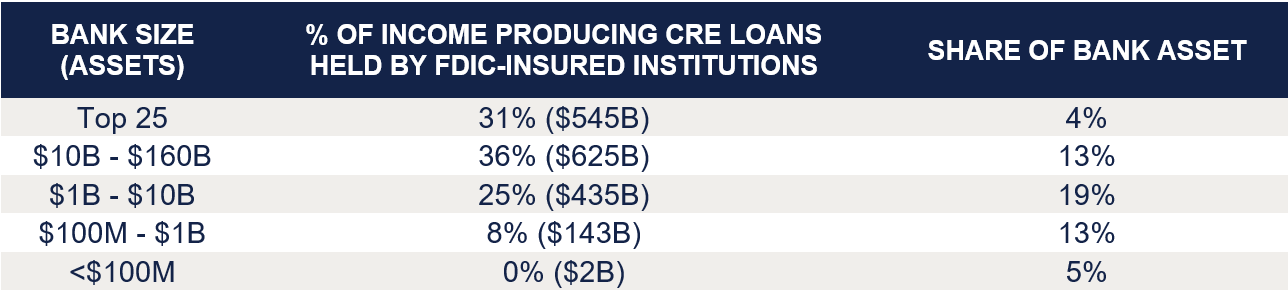

- We can look at banks’ exposure to CRE debt to address default risk and its impact on banks and the economy. If we only consider income-producing CRE (apartments, office, retail, and industrial), there is $4.4 trillion outstanding in CRE mortgages, and FDIC-insured institutions hold $1.75 trillion (around 40%) of those loans.2 As discussed earlier, while office and retail CRE are under stress, other CRE property sectors are faring quite well, so one shouldn’t assume that all CRE debt is under the same strain.

- If CRE does experience a significant hit, the government or Federal Reserve (Fed) would likely step in to prevent systematic contagion, similar to how they helped when Silicon Valley Bank and First Republic failed earlier this year.

What to Keep an Eye On

As we mentioned earlier, the CRE market is large and complex. Some property sectors are thriving, and some are strained. Some sectors could see a decrease in property values and an increase in loan defaults from the rise of interest rates, which could further stress the banking sector. However, while significant defaults on CRE debt and bank contagion are possible, they’re not the base-case outcome. Instead, we will likely see an increase in defaults—especially in regions of the country where the population is decreasing—but the crisis scenario depends on many factors and assumptions that may not materialize or hold true.

These bleak predictions also overlook the diversity of the CRE market and banking sector, as well as the data and evidence that contradicts or, at a minimum, challenges them. Therefore, while it is prudent to be aware and prepare for the potential risks and challenges in the CRE market and the banking sector, the data doesn’t indicate an imminent meltdown in CRE as much as it could be a slow-burning issue for years to come.

As with all investments, we recommend diversification. If you want to invest in CRE, diversify across different locations and property types and have a long-term perspective. Investing in real estate carries risks, and it’s important to carefully evaluate each opportunity based on your risk tolerance, financial goals, and investment strategy.

As we continue to monitor the situation for our clients, our real estate funds are less than 5% of any solution and those funds are diversified among different property sectors. Market dislocation can create attractive opportunities, so we are evaluating private market managers who have experience investing in similar environments. If you have additional questions, please reach out to your Blue Trust advisor or contact us at 800.987.2987 or email blog@bluetrust.com.