Understanding Private Credit: Risk, Liquidity, and Reality

Executive Summary

Private credit faces real risks, including credit losses, limited liquidity, and less transparency than public markets. Those risks should not be dismissed. But they also should not be evaluated based on headlines alone.

In our view, a better approach is to assess private credit through the lens of underwriting discipline, portfolio construction, manager quality, fund structure, and investor time horizon. When viewed that way, the opportunity set looks more nuanced than much of the recent media coverage implies.

That distinction matters when evaluating managers such as Blue Owl. While risks remain, the available data suggest that Blue Owl’s direct lending strategies are positioned more favorably than broad concerns around private credit might indicate.

We do not think investors should ignore the risks in private credit. However, it’s equally important not to confuse risk with panic, or headlines with thoughtful analysis. For investors with an appropriate time horizon, a clear understanding of private credit’s risks and illiquidity, and a well-diversified portfolio, we believe private credit can be an attractive opportunity.

Understanding Risks in Private Credit

Past performance is not indicative of future results and investing involve risks, including the loss of principal.

We see disclosures like this all the time, but strong recent returns can make risk feel abstract. The goal of investing is not to avoid risk altogether; it is to understand which risks you are taking and whether you are being compensated for them. “Risk” comes in a variety of different forms but fundamentally speaking, higher returns require bearing more risk.

With private credit still in the spotlight, we believe investors are better served by a more balanced perspective than many recent headlines provide. Our view is straightforward: Private credit carries real risks, but those risks should be evaluated with fundamental data and within the context of an appropriate time horizon.

This piece is meant to address questions advisors and investors are asking today: What are the real risks in private credit broadly? How should we think about Blue Owl’s direct lending funds specifically?[1] For a deeper primer on the asset class and the recent media narrative, please see our Understanding Private Credit: Dispelling the Doom and Gloom blog post published last November.

Blue Owl specializes in senior secured, direct lending to large, sponsor-backed companies. In simple terms, Blue Owl lends to large companies (generating on average $1B+ in revenue and $250MM+ in EBITDA) backed by private equity firms, with priority repayment in the event of bankruptcy.

These loans are floating rate, meaning they adjust with interest rates. Over the past three years, a higher rate environment and low default levels have contributed to 8%+ annualized returns for Blue Owl’s private , with two out of three exceeding 10% annualized―compared to less than 5% return for the Bloomberg Aggregate Bond Index.

These results help explain private credit’s growing popularity. But investors should not confuse strong recent returns with low risk. The right question is not whether private credit is risky―it is―but which risks matter most, how they are being underwritten, and whether investors are being adequately compensated to bear them.

Credit risk

At the most basic level, private credit borrowers carry more risk than those in Treasuries, investment-grade corporate bonds, or other high-quality fixed income. The individual companies borrowing from private credit lenders aren’t typically rated by agencies like S&P, Moody’s, or Fitch. If they were, most would likely fall into the “sub-investment grade” or “high yield” or “junk” category (all synonymous terms) due to their smaller size, debt levels, and higher probability of default. This elevated credit risk is a primary driver of higher yields.

Supporters of private credit argue that this added risk can be mitigated through specialized underwriting, tighter lender protections, direct access to company information, and the ability to structure loans for speed, certainty, and confidentiality. In other words, part of the yield premium may reflect lender skill and market structure, not just weaker credits.

Critics point out that recent default experience may understate the true level of risk. Payment-in-kind toggles, amend-and-extend transactions, and a prolonged period of benign credit conditions may have delayed―rather than eliminated―underlying stress. They also note that increased competition for deal flow could weaken underwriting discipline at the margin.

Transparency & Valuation

By nature, private credit is less transparent than public credit. The underlying borrowers are usually private companies, so their financials are not disclosed as broadly as public issuers, and the loans themselves are not priced continuously in public markets. As a result, investors may have less transparency into how these investments are performing and the risks involved.

Proponents of private credit suggest this is not simply an information gap. In many cases, lenders have access to detailed private information that public markets do not, which can enhance underwriting and more accurately determine value. They also note that borrowers often prefer private credit precisely because it offers confidentiality, tailored structuring, and reduced exposure to market volatility. Finally, these loans are independently audited and valued.

Critics, however, view reduced public transparency as a meaningful tradeoff. More disclosure can help investors detect fraud earlier, and market pricing can sometimes identify changes in value more quickly than periodic private marks. That does not mean private valuations are inaccurate, but it does require investors to be comfortable with slower price discovery.

Liquidity

Liquidity has received increased attention recently. Depending on the fund structure, investors may have limited or no ability to exit on demand. That tradeoff was easier to ignore when returns were strong and fear was low, but it becomes much more visible when headlines raise concerns about a downturn, defaults, or forced selling.

Supporters of private credit view redemption limits as a structural feature, not a flaw. These provisions help funds remain open for new investment and can benefit investors who prefer not to lock up capital for a defined period of 8-10+ years. Limited liquidity can also protect remaining investors, as it prevents the manager from becoming a forced seller.

Critics have not seen it this way. They argue that redemption restrictions can feel benign until investors actually want access to their capital. In those moments, limits can be interpreted as a loss of control or even a signal that something is wrong.

Evaluating of Blue Owl in Light of These Risks

This broader framework highlights the importance of evaluating Blue Owl on its own merits, not based on generalizations about private credit. The firm manages over $307 billion ($158B just in credit), has over 1,300 employees, and is rated BBB+ by Fitch. Since inception in March 2016, Blue Owl’s average annual net loss rate of approximately 0.08% compares favorably with about 0.35% for other senior direct lenders and roughly 1.4% for high-yield bonds over the same period. (Source: SP LCD, Cliffwater, JP Morgan).

Looking specifically at Blue Owl Credit Income Corp.(OCIC), one of our most widely used funds, the portfolio includes 354 companies diversified across industries, with each position representing less than 2% of the portfolio. About 93% of those loans are senior secured, and the average loan-to-value is 40%―meaning borrowers would have to lose more than half of their value before the loan is impaired. Investments on non-accrual status represent approximately 1% of the portfolio. Since inception (March 2021 through January 2026), the fund has generated a 9.52% annualized return.

These are strong statistics and, in our view, reflect disciplined underwriting and portfolio management. But they should not lead investors to overlook the risks. Competition in direct lending has increased, and a full modern credit cycle has yet to play out in private markets. Defaults have been relatively low and are likely to rise over time.

Blue Owl is not risk-free, but the current data suggests a disconnect between how the fund has performed and why some investors are choosing to exit.

The same balanced approach applies when evaluating the Blue Owl Technology Income Corp. (OTIC). OTIC is similar to OCIC, but with greater concentration in software and technology-related borrowers. That concentration has drawn more scrutiny given artificial intelligence (AI) and its potential to disrupt incumbent software businesses.

Those concerns are not unfounded, but current fund data does not point to broad distress. OTIC’s borrowers are generating an average of $1.8 billion in revenue and $388 million of EBITDA, with an average loan-to-value of 34%. The portfolio has no investments on non-accrual. Since inception (May 2022 through January 2026), the fund has generated 10.43% annualized return, and elevated redemption requests were met.

A recent transaction involving OBDC II, OBDC, and OTIC is also worth noting. After the previously contemplated merger of OBDC II into OBDC was called off, Blue Owl pursued an alternate path to generate liquidity―selling approximately $1.4 billion of direct lending assets to four large North American pension and insurance investors at roughly fair value (about 99.7% of par).

In our view, that outcome matters for two reasons. First, it provided meaningful liquidity to OBDC II investors and supports Blue Owl’s stated plan to close the fund and return capital to investors. Second, the ability to sell assets near carrying value offers some validation that recent portfolio marks were broadly in line with market-clearing levels.

This transaction does involve a tradeoff. Investors lose the option to submit full or partial redemption requests, even though redemptions were never guaranteed. Still, the transaction is intended to support a more orderly path to liquidity.

Our takeaway is not that the concerns are baseless, but that broad narratives often compress very different managers, underwriting standards, and fund structures into one story. That framing can be misleading, particularly when the available data for Blue Owl remains comparatively strong.

Even so, to be intellectually honest, we should acknowledge that markets are forward-looking. The key question for investors is not whether recent results have been strong, but where the next pressure points are most likely to emerge. Let’s unpack those considerations next.

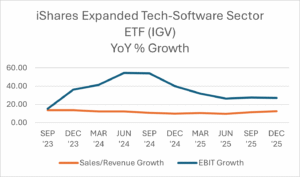

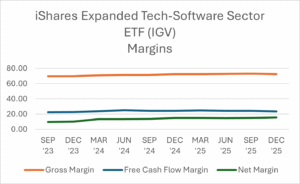

AI Disruption

AI is one of the most important developments for software investors, and it should be taken seriously. The market has sold off in more of a ready, fire, aim mentality. Some software companies will be disrupted, but we do not believe the most extreme version of the bear case―that AI will quickly replace most incumbent software vendors―is the base case.

In practice, software replacement is often slowed by switching costs, entrenched integrations, compliance requirements, customer relationships, and the simple fact that many enterprise systems are more difficult to replace than commonly assumed. The data below also suggests that while valuations have been priced significantly lower, operating fundamentals have remained resilient.

Source: FactSet

Source: FactSet

In our view, AI is a more meaningful medium-term underwriting variable than an immediate portfolio impairment risk for diversified, senior-secured lenders. In private credit, the near-term risk appears more limited given the durability of cash flows from existing software businesses.

As a result, we are not overreacting to AI risk in private credit by broadly dismissing funds like OTIC. We do think the implications may be more significant for equity investors as the long-term impacts are highly uncertain and it remains unclear whether recent valuations post-selloff are oversold or indicative of a changing paradigm for valuing SaaS businesses.

Credit Risk

Predicting the timing and shape of the next credit downturn is nearly impossible. We do expect defaults in private credit to rise at some point―that is part of the asset class―but the timing is difficult to call. When the Federal Reserve began aggressively raising rates in 2022, many investors expected a broad credit crisis because borrowing costs were moving sharply higher. That did not happen. Instead, private credit went on to post some of its strongest annual returns.

Private credit is not immune to experiencing losses. Therefore, we believe the most effective way to manage that risk is through appropriate time horizon alignment. Private credit should be held for a minimum of three years, and preferably longer. Capital needed within a shorter timeframe is generally better allocated to cash and/or traditional fixed income with lower credit risk.

Illiquidity Risk

Investors should assume that redemptions are limited and may be capped. That is one of the key tradeoffs in semi-liquid vehicles versus traditional daily liquidity or closed-end structures.

Liquidity constraints tend to matter most when fear rises, not when conditions are calm. One of the most effective ways to manage that risk is through diversification―not only across borrowers, but also across managers, fund structure, liquidity terms, and strategies. While this will not eliminate liquidity pressure in a stressed environment, it can improve flexibility and reduce the risk that a single gate or manager drives the entire experience.

At a broader level, investors should also be thoughtful about their total allocation to illiquid alternatives. There is no single right answer, but suitability, cash flow needs, and behavioral tolerance all matter. As a general framework, we often discuss a range of roughly 5% to 25% of a total portfolio, depending on the investor.

Conclusion

Private credit deserves neither blind enthusiasm nor blanket skepticism. It deserves thoughtful analysis. The asset class can offer attractive income and downside protection, but only if investors are clear-eyed about the tradeoffs: higher credit risk than traditional fixed income, less transparency than public markets, and liquidity that is limited by design.

We believe the right response to today’s headlines is not to treat all private credit the same. Manager quality, portfolio construction, underwriting discipline, fund structure, and investor time horizon matter significantly. In our view, private credit carries real risks, but those risks should be evaluated with the appropriate data, relative to other opportunities available, and within the appropriate time horizon.

Applying that framework to Blue Owl leads us to a more constructive conclusion than much of what the recent media coverage suggests. Private credit involves risk and there is no guarantee that future results will mirror the past. However, based on the data currently available, Blue Owl’s direct lending strategies appear better positioned than generic private credit narratives imply.

[1] Blue Owl offers other strategies as well.