Q1 2026 brought geopolitical tension and market volatility from Middle East escalation, trade policy shifts, and concerns about AI disruption and private credit risks. Despite headlines around Venezuela, Fed leadership changes, and labor market uncertainties, underlying economic fundamentals remained stable with resilient financial markets.

Executive Summary

The first quarter of 2026 produced a wide range of geopolitical and market-driven developments, yet financial markets generally held steady. While events in Venezuela, trade policy shifts, and evolving Federal Reserve (Fed) expectations contributed to uncertainty, the most meaningful disruption came from the escalating conflict in the Middle East, which drove a sharp rise in energy prices and renewed inflation concerns.

At the same time, investor attention shifted toward risks tied to artificial intelligence (AI) and private credit. Private credit concerns and rapid AI driven labor disruption fears gained traction, but underlying trends point to stable fundamentals and limited evidence of broad economic deterioration.

International equities continued their outperformance relative to the U.S., particularly during the first two months of the quarter, as enthusiasm around megacap U.S. technology moderated.

Overall, despite recent daunting headlines, the core economic backdrop remains stable. We believe a diversified portfolio, grounded in long-term discipline, remains well positioned to navigate both near-term volatility and evolving structural trends.

Blue Trust Insights

The opening months of 2026 were filled with headline-grabbing events that markets moved through with notable resilience. In January, the Trump administration authorized a military operation in Caracas that led to the capture of Venezuelan leader Nicolás Maduro, who was subsequently brought to the U.S. to face longstanding federal charges. Soon after, reports of a possible U.S. takeover of Greenland raised concerns about tensions within NATO. During the same period, Fed Chair Jerome Powell was reported to be under criminal investigation, and President Donald Trump announced his long-awaited Fed chair selection, Kevin Warsh, at the end of the month.

February brought a significant Supreme Court ruling that overturned tariffs imposed under emergency authority, a central element of the administration’s trade approach, raising the possibility of refunds to corporations for previously collected duties. By late February, a joint U.S.–Israeli strike on Iran escalated tensions in the Middle East, disrupting the Strait of Hormuz, a key trade corridor that handles roughly 20% of global energy flows, and sending crude oil prices sharply higher.

Domestically, job growth continued to cool while layoffs remained subdued, reinforcing the “no hire, no fire” labor dynamic. Meanwhile, rapid improvements in AI capabilities pressured software stocks and prompted some investors to reassess private credit exposure to the sector.

Private Credit

Private credit was already in the spotlight, and fears escalated in the first quarter as investors began to question the asset class’s exposure to firms that may be radically altered by AI, potentially leading to higher default risk. Private credit carries real risks, including credit losses, limited liquidity, and less transparency than public markets. These risks should not be dismissed, but they also should not be evaluated based on headlines alone.

In our view, a more effective approach is to assess private credit through underwriting discipline, portfolio construction, manager quality, fund structure, and the investor’s time horizon. When viewed through those lenses, the opportunity set appears more nuanced than recent media coverage suggests.

Investors should remain attentive to the risks but avoid the tendency to equate uncertainty with deterioration or headlines with analysis. For our full perspective on recent private credit developments, click here.

AI

Social media has radically accelerated the dissemination of news, turning stories that once took days to spread into narratives that gain momentum within minutes. This dynamic was on full display in the first quarter, when a dystopian AI hypothetical scenario—imagining rapid AI adoption replacing large portions of white collar labor went viral and drove a weeks long pullback in software and payments stocks, as well as alternative asset managers with exposure to software firms. The report suggested that intermediary-heavy industries, such as finance and software, could see their competitive advantages weaken as AI tools become cheap and ubiquitous, lowering barriers to entry and enabling AI-native firms to challenge incumbent pricing power.

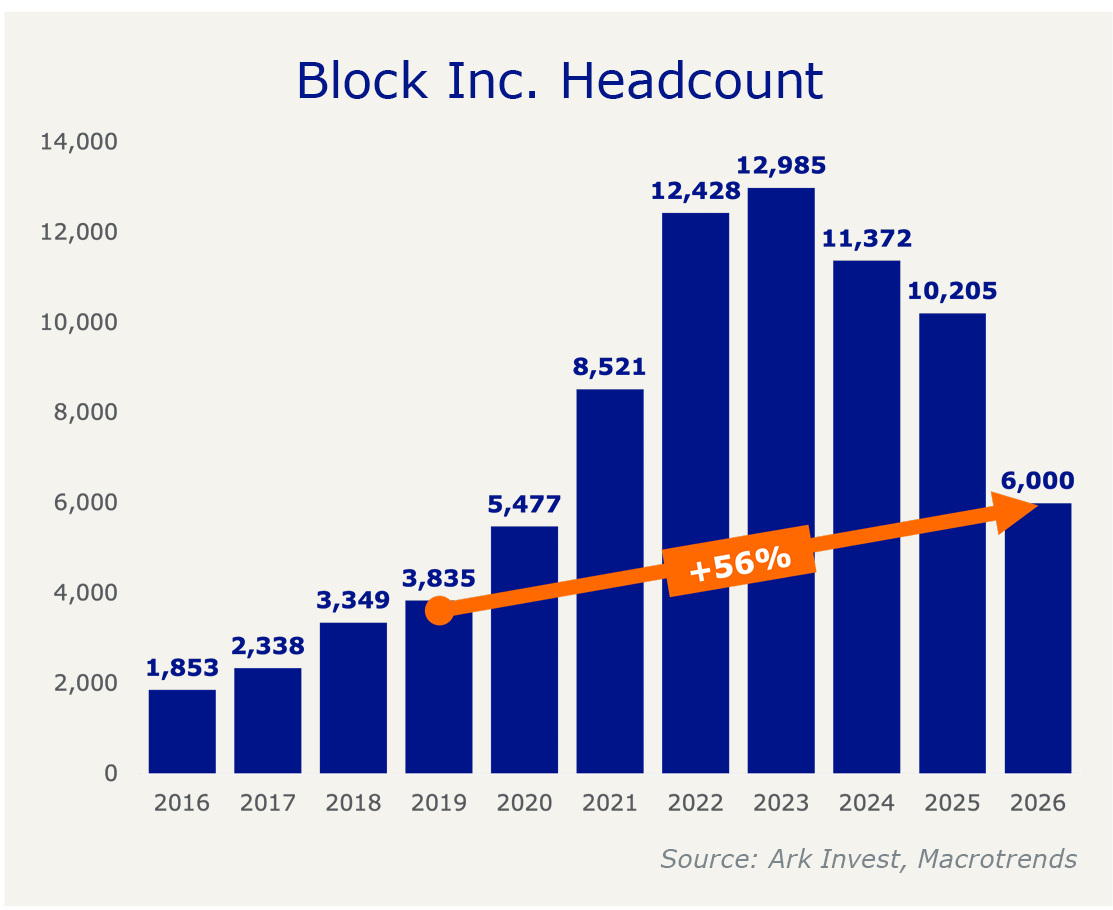

In the days following the report, Block Inc.—the parent company of Square and Cash App—announced plans to cut 40% of its workforce. Some viewed this as early confirmation that AI driven job losses are accelerating. While AI is likely to reduce labor in certain areas over time, we do not view this development as evidence of broad, imminent displacement of white collar roles.

Even after these reductions, Block’s workforce remains roughly 60% larger than it was in 2019. It is also worth noting that Jack Dorsey, Block’s cofounder and CEO, previously cofounded Twitter, where the workforce was famously cut by 80% following Elon Musk’s acquisition of the company in 2022. This context has led some analysts to suggest that Block may simply be unwinding post pandemic over-hiring rather than responding solely to AI-driven changes.

Further complicating the narrative, job postings for software developers—often viewed as among the most exposed workers to AI—are up 15% year over year, even as overall job postings have declined. We are not suggesting that every announcement of AI related layoffs is exaggerated or untrue. However, it is important to consider that companies that accelerated hiring during one of the most economically tumultuous periods in history may now be adjusting the size of their workforce, with AI serving as a clear and compelling explanation for those decisions. Dire labor market predictions rely on the assumption that AI will be able to complete a broad array of tasks in the future. Given how difficult it is to forecast even near-term employment data, predictions of widespread unemployment should be viewed with appropriate caution.

While we see limited evidence of broad AI driven labor disruption today, the future remains uncertain. In our view, new technology is more likely to augment human labor than replace it. For example, the introduction of Microsoft Office was a complement to office workers rather than a substitute.

Beyond cost considerations, AI adoption will likely face hurdles such as regulation and potential consumer pushback. Some jobs will inevitably be displaced, but new ones will emerge, as they have with every major technological shift. Notably, most current occupations did not exist prior to 1940.

We believe markets and workforces adapt over time, ultimately supporting higher productivity, stable or improving margins, rising wages, and increased demand for products and services that are difficult to imagine today.

AI and the Economy

According to the international research firm Gartner Inc., global AI spending is expected to reach $2.5 trillion in 2026, up 44% from last year. Recently, investor focus has expanded beyond megacap AI leaders to companies positioned at critical bottlenecks in the AI build-out, such as memory suppliers. As AI models have grown larger and are increasingly used in real-time applications, demand for memory has surged, lifting stock prices and leaving some suppliers effectively sold out for the year. While U.S. memory-focused firms have seen strong share price appreciation, the trend is global. Major players in South Korea and Japan are also contributing to market strength, extending international outperformance that began last year.

Within the U.S., market performance has begun to broaden as investor enthusiasm around AI appears to be cooling. Mentions of AI on S&P 500 earnings calls hit a record in the fourth quarter. Yet, companies that mentioned AI have recently lagged those that did not. Firms continue to report strong results and expand AI related investment plans, but the market seems more cautious toward large and rising capital expenditures that could pressure cash flows. Indeed, the relative underperformance of the Magnificent Seven stocks compared to the equal-weight S&P 500 suggests that market participation is broadening beyond megacap names.

Iran Conflict

While most first quarter events drew limited market reaction, the joint U.S.–Israeli strike on Iran was a notable exception, prompting a multi-week decline in global stock and bond markets amid retaliatory missile attacks. Ayatollah Ali Khamenei, who had ruled Iran since 1989, was killed in the initial strikes.

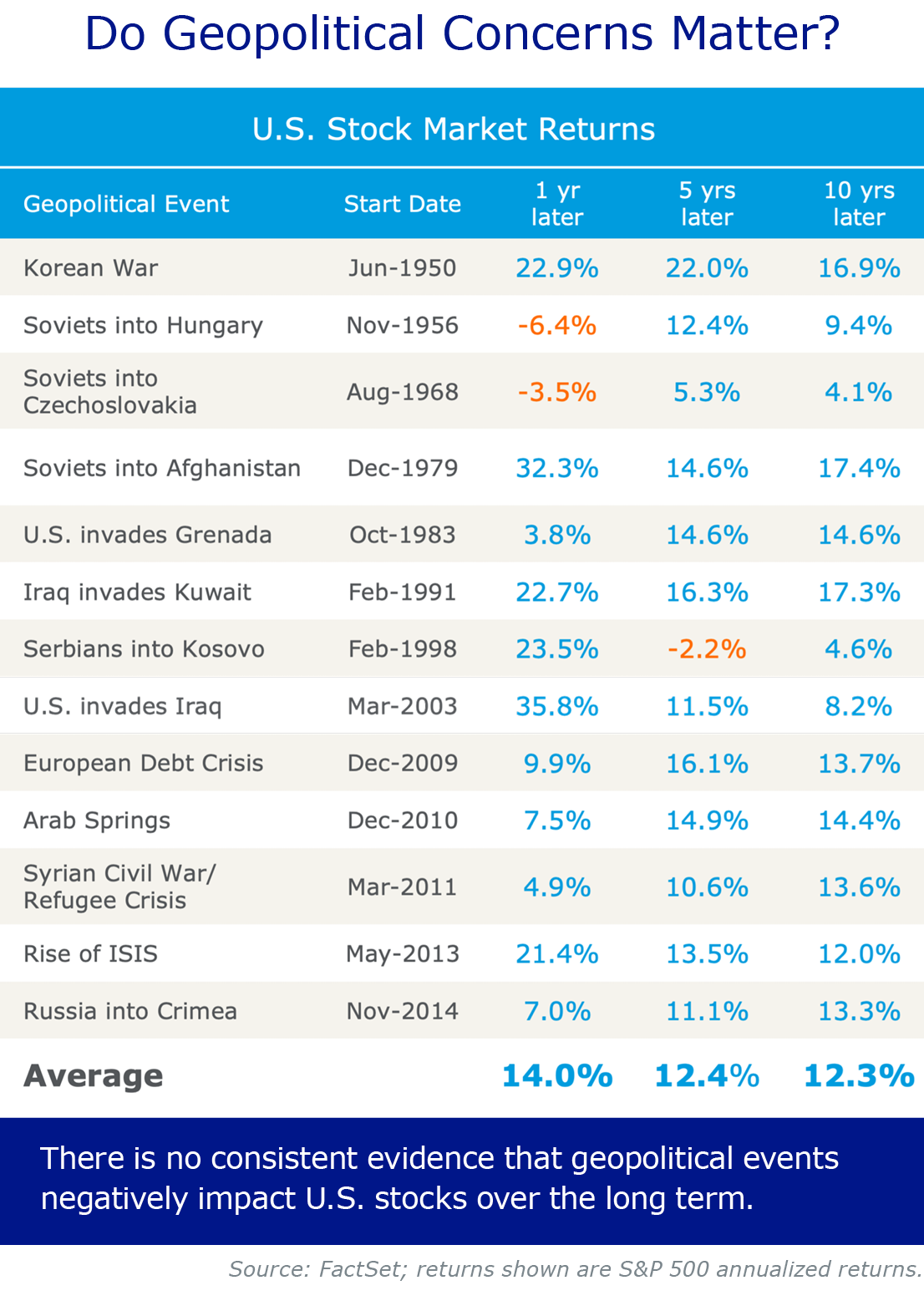

Geopolitical shocks have historically had limited and short-lived effects on the U.S. economy. As a net energy exporter, the U.S. is relatively insulated from short-term growth risks tied to energy price spikes, although a prolonged conflict or sharp market correction could still weigh on consumers. Because consumer spending is primarily driven by higher income households, a persistent downturn in equity markets would likely dampen spending among top earners and slow overall economic activity.

A durable and substantial rise in shipping costs could add pressure to core goods inflation. However, we expect the Fed would likely look past a temporary, supply-driven energy shock unless it caused a meaningful rise in consumer inflation expectations.

Iran Conflict: Impact on International and Emerging Markets

With the de facto closure of the Strait of Hormuz, oil and natural gas prices surged. West Texas Intermediate crude jumped more than 35%, marking its largest one week gain since 1983, and briefly exceeded $110 per barrel for the first time since Russia’s invasion of Ukraine.

As crude shipments halt and storage in the Persian Gulf nears capacity, market concerns are likely to increase the longer the disruption lasts. A prolonged shutdown would make it more difficult for Gulf producers to restore normal output, further amplifying global energy pressures.

While the U.S. sources only about 7% of its crude oil imports from the Strait, higher gasoline prices show that it’s not fully insulated. Europe and Asia are far more exposed as net energy importers. For Europe—already strained by reduced access to Russian energy—a sustained spike in energy prices would place additional pressure on both growth and inflation.

More than 80% of the crude that transits the strait flows to Asia, making it the largest importer of Gulf region oil. Japan and South Korea, for example, rely on the Gulf for roughly 90% and 70% of their oil imports, respectively.

South Korea entered 2026 as one of the world’s top performing equity markets, driven largely by AI linked tech giants Samsung Electronics Co. and SK Hynix Inc., which together account for more than 40% of Korea’s market capitalization. The recent conflict triggered a sharp pullback in Korean equities and declines across other developed international and emerging markets. Still, Korea’s existing energy reserves should help mitigate near-term supply issues unless the disruption becomes prolonged. Other Asian economies face similar vulnerabilities given their reliance on imported energy. Japan’s sizable reserves offer nearly a year of cushion, but an extended shock would still strain regional growth. In the interim, some economies have turned to coal as a temporary alternative.

Based on forward earnings expectations, emerging market valuations are roughly in line with their 10-year averages, and earnings forecasts are improving, led by strong growth in Korea. Looking beyond near term uncertainty, we believe AI driven growth and market reforms in South Korea—along with continued reforms and supportive fiscal policy in Japan—should continue to support equities once energy markets stabilize. Although the conflict briefly strengthened the dollar in a typical flight-to-safety trade, we expect the still overvalued dollar to enhance international equity returns over the longer term.

Iran Conflict: China

Some observers have suggested that recent U.S. actions in both Venezuela and Iran may reflect a broader effort to respond to China’s growing economic and strategic influence. China has developed deep ties with both countries, including a 25-year cooperation pact with Iran, signed in 2021, that includes significant investment in energy, infrastructure, and banking.

From that perspective, limiting China’s access to cheap energy and influence in South America and the Middle East would align with U.S. strategic interests if China is viewed as a primary competitor. In that context, efforts to weaken or replace governments aligned with China could be seen as a way to limit its influence without triggering direct conflict.

However, as noted last quarter, China remains a major producer and the world’s leading refiner of rare earth minerals, which are critical to global supply chains. This reality underscores the potential for renewed tensions if geopolitical dynamics continue to evolve, particularly given the strategic importance of these materials to the U.S. and its allies.

At the same time, China’s relationships in both regions are complex and resilient. Beijing maintains long-standing economic ties with Venezuela, including energy trade and financing arrangements, and continues to play a measured, largely nonmilitary role in the Iran conflict. President Trump has indicated that Venezuela may continue supplying oil to China, suggesting a full disruption of energy flows is unlikely.

Despite recent tensions, diplomatic engagement appears to remain intact. Trade representatives from both countries continue to meet regularly, and China still plans to host President Trump in Beijing, with the White House confirming the trip has been pushed to May as events in the Middle East unfold.

Conclusion

The duration of the conflict in Iran will likely be a key factor shaping markets in the months ahead. A short disruption would likely allow for a quick market recovery, while a prolonged conflict could have a more meaningful impact on inflation and growth. If energy prices stay elevated, a hawkish Fed would likely delay rate cuts until clearer disinflationary trends emerge.

Looking beyond near-term uncertainty, we expect the AI driven momentum that is supporting emerging and developed international markets to continue. Asia is the most exposed to the current energy shock, yet the region still benefits from strong secular tailwinds.

Over the past year, an improving growth outlook, weaker dollar, and attractive valuations have helped international market performance. We believe the long-term case for emerging markets remains intact and should reassert itself once geopolitical pressures ease.

History shows global events rarely leave lasting marks on stock performance and often create buying opportunities. If energy costs do not rise meaningfully or persistently, growth and earnings should remain resilient. While recent headlines are unsettling, this environment underscores the importance of a thoughtful financial plan and a well-diversified portfolio that is positioned for future opportunities.

Market Recap

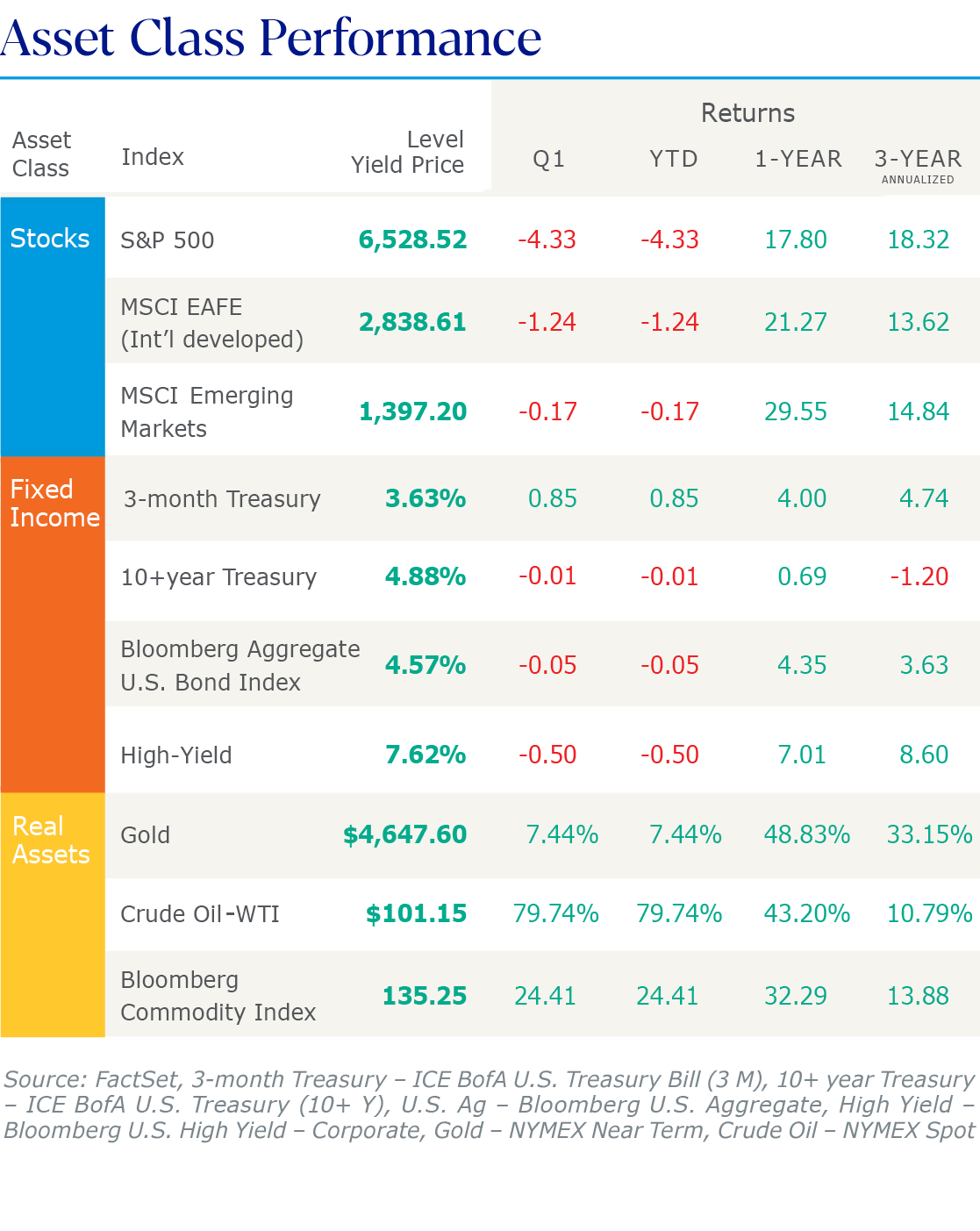

U.S. stocks were essentially flat through the first two months of the quarter before declining in March as the Iran conflict began, ultimately finishing the quarter down 4.3%. Developed international and emerging markets started the year strongly, outperforming the S&P 500 by 9% and 14%, respectively, before the gap narrowed as energy-related concerns weighed more heavily on international markets.

Gold continued its impressive run, climbing 22% before giving back most of its year-to-date gains, though it remains up 47% over the past year. Commodities also advanced early in the quarter, with oil prices becoming increasingly volatile as investors reacted to developments in the Middle East. Bond markets were relatively flat.

Market expectations for Fed policy shifted noticeably over the first quarter. They began the year anticipating two rate cuts, but rising energy prices and renewed inflation concerns prompted policymakers to take a more cautious outlook. By late March, expectations shifted to no rate cuts in 2026, with a 1% probability of a rate increase, although Fed projections still suggest one possible cut this year.

Looking for personalized guidance?

Our advisors bring financial expertise and biblical wisdom together to guide the decisions shaping your future.